Fairfax Financial: Necessity for Human Excellence in Insurance via 1985 - 1999 Letters

"Fairfax continues to attract very good people – the best sign I know of success in the future.” - Prem Watsa

The following is an investing article for OMD Journal. Keep in mind I may own or have owned the company discussed. None of this is investment advice, do your own due diligence.

Find the archive of companies and people explored here

Today, Fairfax Financial Holdings has a market capitalization of ~$16b CAD. In 2020, it had ~$19b in sales on an asset base of $74b and shareholder equity of $12b. But instead of speaking of today’s operations, I will be delving into Fairfax’s letters from 1985 to 1999 and pulling out lessons on decentralization, discipline and the importance of people in insurance from Prem Watsa, CEO and Chairman of Fairfax.

First, you might wonder if this holding company in Toronto, Canada, is even worth a look. Throughout its first 14 years, Fairfax’s average return on equity (ROE) was 19.2% and its book value per share compounded at 40% per annum. Using these two metrics as benchmarks for assessing intrinsic value for the business, the stock price compounded at 36% per year. That, my friends, are impressive results for any company, let alone a boring insurance company.

By 1999, there were only two other Canadian companies that had compounded their stock price at a faster annual rate over the 14 year period. South of the border, there were eight companies in the U.S. that had compounded faster.

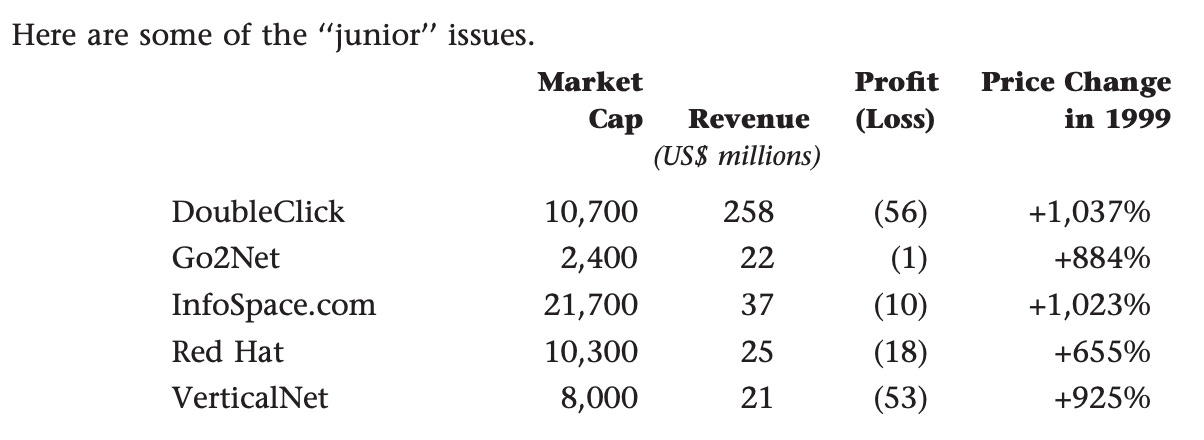

Keep in mind, in 1998, there were only two U.S. companies that had compounded faster over a 13 year period. Fairfax saw a near 50% decline in its share price in 1999—the year when Dotcom companies traded at absurd price levels:

Even Amazon traded at 14x sales. This was before they had AWS and before any operating cash flows that showed possibilities of Amazon's model even working. Today, it trades around ~4x sales as the largest cloud and e-commerce business in the world.

This was all context to lay the foundation for Prem Watsa and the long-term track record he established operating a boring insurance holding company after rescuing it from bankruptcy.

Watsa’s Decentralized Holdco

Prem Watsa, the CEO and Chairman of Fairfax Financial Holdings, was a name most Canadian investors learned early in our journeys. The learning process started with a budding fan-ship of Warren Buffett and Berkshire Hathaway. Thanks to the death of privacy and birth of connectivity, it wasn't a reach for Google to start suggesting articles about the “Warren Buffett of Canada."

Though both companies shared having a smart investor at the helm, they shared a similar start as well. Both Berkshire Hathaway and Fairfax Financial were failing businesses that were acquired by the future capital allocators (i.e. Buffett and Watsa). While Berkshire Hathaway started as a textile operation that morphed into an insurance business, Fairfax started in insurance—trucking insurance to be specific.

Watsa took over Fairfax, which was called Markel Financial Holdings at the time, in 1985. This was about 20 years after Buffett’s takeover of Berkshire.

The Indian-Canadian billionaire—not back then but he is today—often wrote of Buffett’s track record and cited how that fact was hope for the burgeoning Fairfax. As Fairfax continued its decades of compounding, Watsa’s letters and the holding company itself became another pond to study. If that wasn’t enough, Watsa citing Buffett and Ben Graham early in his annual letters would’ve attracted investors who smelled a possible cloner.

It wasn’t just Watsa’s presence in the investing interwebs or books. I felt Watsa and Fairfax’s invisible hand over Canada’s investing community when I began my journey. From mentors, friends, colleagues to other institutional investors I would meet from a cold call, many had—in some way—floated around Fairfax and Watsa’s circle of influence. Some worked with Watsa, were hired into his subsidiary, were mentored by him or received a scholarship from him on their own investing journey.

Similar to how I had never read all of Buffett’s letters despite my foray into value investing, same was the case with Watsa’s letters. That made the Fairfax annual letters a natural set to read. But what further prompted my curiosity was how Watsa described Fairfax’s structure in their Guiding Principles.

This reminded me of Berkshire’s decentralized structure and wondered how Fairfax went about building its organizational culture. While Buffett’s letters dove into Berkshire’s culture, their managers, and lessons from various parts of operations, a few key differences jumped out to make the Fairfax letters a different experience for me.